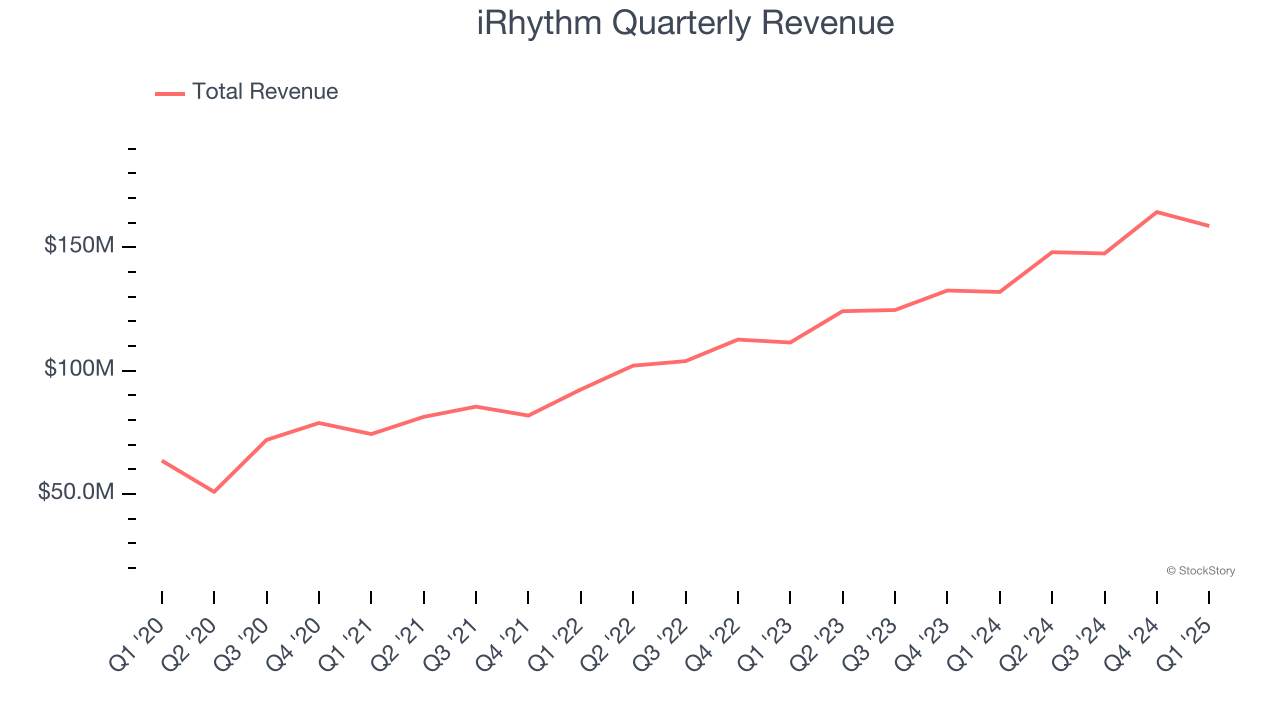

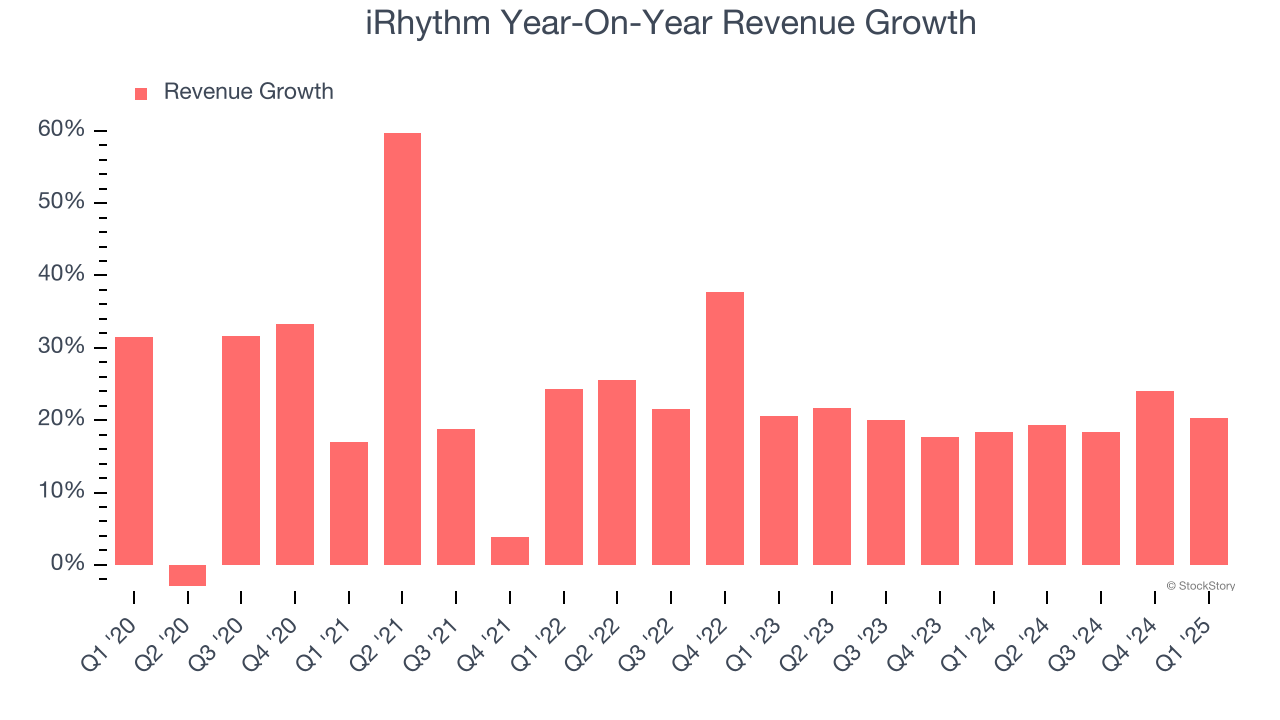

Medical technology company iRhythm Technologies (NASDAQ:IRTC) reported Q1 CY2025 results beating Wall Street’s revenue expectations, with sales up 20.3% year on year to $158.7 million. The company’s full-year revenue guidance of $695 million at the midpoint came in 2% above analysts’ estimates. Its non-GAAP loss of $0.95 per share was 1.5% below analysts’ consensus estimates.

Is now the time to buy iRhythm? Find out by accessing our full research report, it’s free.

iRhythm (IRTC) Q1 CY2025 Highlights:

- Revenue: $158.7 million vs analyst estimates of $153.6 million (20.3% year-on-year growth, 3.3% beat)

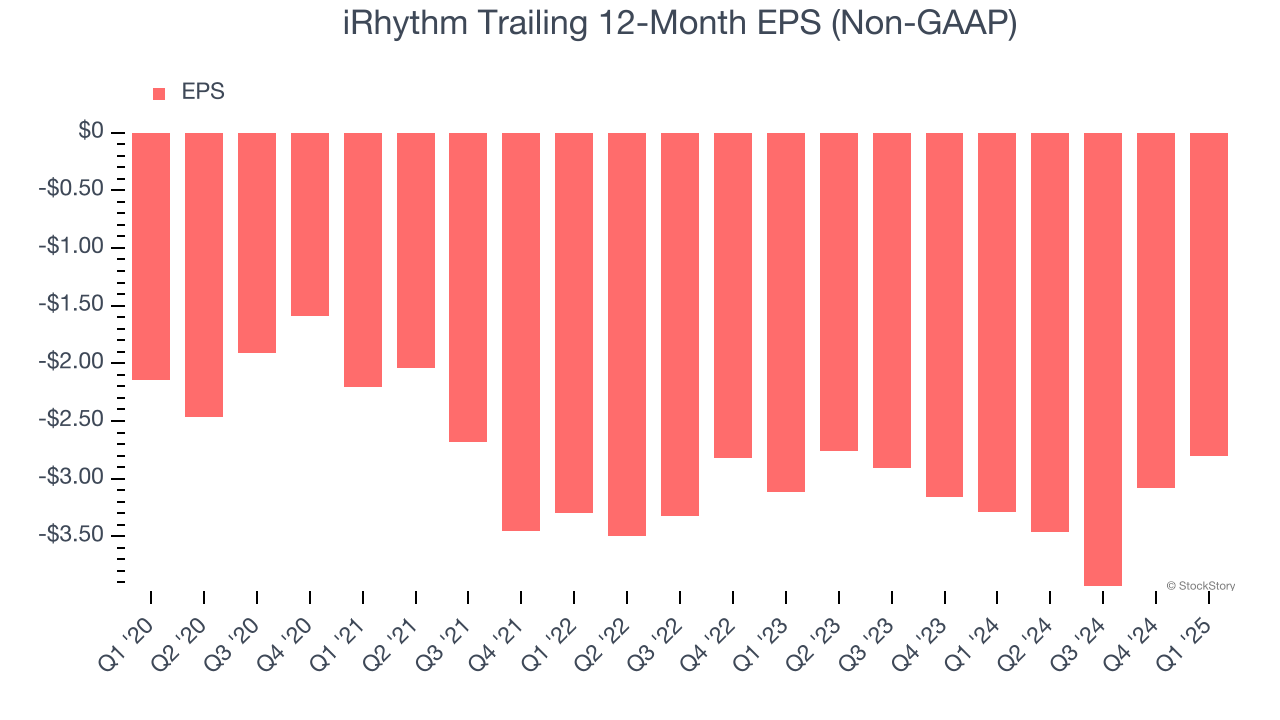

- Adjusted EPS: -$0.95 vs analyst expectations of -$0.94 (1.5% miss)

- Adjusted EBITDA: -$2.64 million vs analyst estimates of -$5.03 million (-1.7% margin, 47.6% beat)

- The company lifted its revenue guidance for the full year to $695 million at the midpoint from $680 million, a 2.2% increase

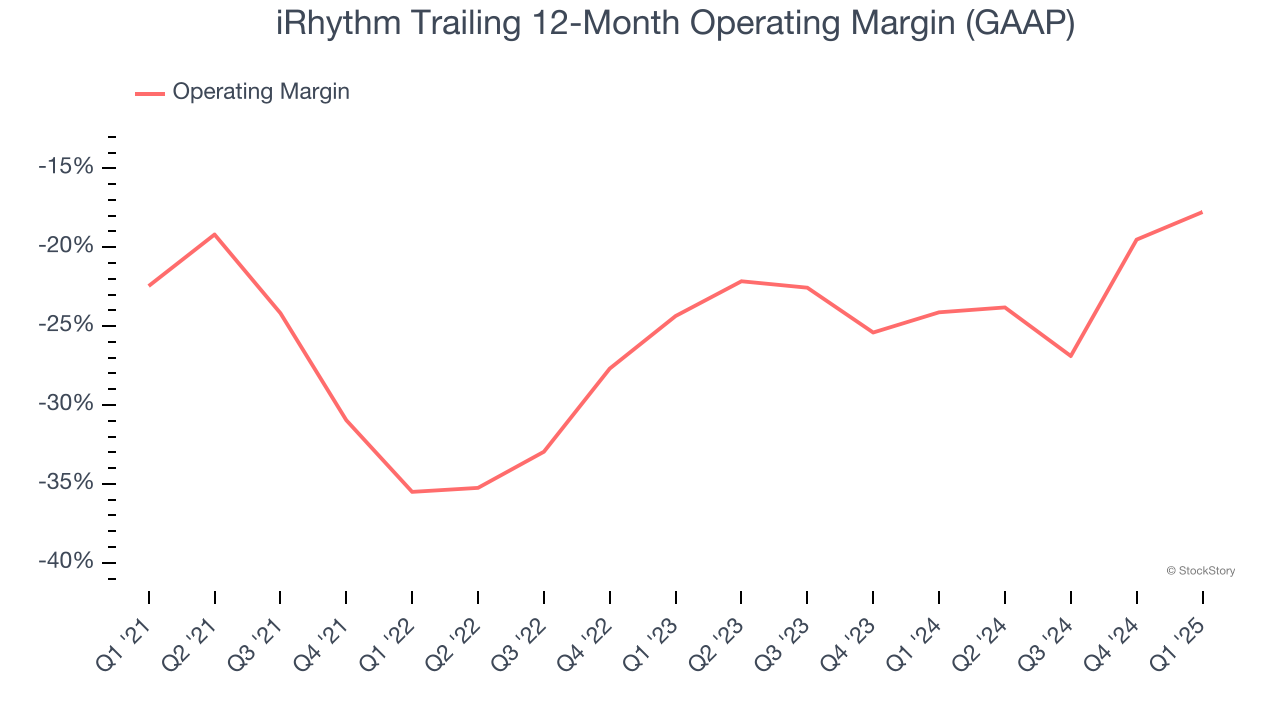

- Operating Margin: -20.5%, up from -28.9% in the same quarter last year

- Market Capitalization: $3.41 billion

"The first quarter of 2025 demonstrated continued commercial momentum, with revenue growth exceeding 20% year-over-year, driven by upstream expansion in the patient care pathway and strength in our Zio AT business," said Quentin Blackford, President and Chief Executive Officer of iRhythm.

Company Overview

Pioneering the shift from bulky, short-term heart monitors to sleek, wire-free patches, iRhythm Technologies (NASDAQ:IRTC) provides wearable cardiac monitoring devices and AI-powered analysis services that help physicians detect and diagnose heart rhythm disorders.

Sales Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, iRhythm’s 21.9% annualized revenue growth over the last five years was excellent. Its growth beat the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. iRhythm’s annualized revenue growth of 19.9% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, iRhythm reported robust year-on-year revenue growth of 20.3%, and its $158.7 million of revenue topped Wall Street estimates by 3.3%.

Looking ahead, sell-side analysts expect revenue to grow 14.4% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is commendable and indicates the market is baking in success for its products and services.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

iRhythm’s high expenses have contributed to an average operating margin of negative 23.9% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, iRhythm’s operating margin rose by 4.7 percentage points over the last five years, as its sales growth gave it operating leverage. This performance was mostly driven by its recent improvements as the company’s margin has increased by 6.6 percentage points on a two-year basis.

In Q1, iRhythm generated a negative 20.5% operating margin. The company's consistent lack of profits raise a flag.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

iRhythm’s earnings losses deepened over the last five years as its EPS dropped 5.5% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, iRhythm’s low margin of safety could leave its stock price susceptible to large downswings.

In Q1, iRhythm reported EPS at negative $0.95, up from negative $1.23 in the same quarter last year. Despite growing year on year, this print slightly missed analysts’ estimates. Over the next 12 months, Wall Street expects iRhythm to improve its earnings losses. Analysts forecast its full-year EPS of negative $2.80 will advance to negative $1.47.

Key Takeaways from iRhythm’s Q1 Results

We enjoyed seeing iRhythm beat analysts’ revenue and EBITDA expectations this quarter. We were also glad its full-year revenue guidance exceeded Wall Street’s estimates. On the other hand, its EPS slightly missed. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 4.6% to $114.01 immediately following the results.

iRhythm may have had a good quarter, but does that mean you should invest right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.