Let’s dig into the relative performance of Rush Enterprises (NASDAQ:RUSHA) and its peers as we unravel the now-completed Q4 vehicle parts distributors earnings season.

Supply chain and inventory management are themes that grew in focus after COVID wreaked havoc on the global movement of raw materials and components. Transportation parts distributors that boast reliable selection in sometimes specialized areas combined and quickly deliver products to customers can benefit from this theme. Additionally, distributors who earn meaningful revenue streams from aftermarket products can enjoy more steady top-line trends and higher margins. But like the broader industrials sector, transportation parts distributors are also at the whim of economic cycles that impact capital spending, transportation volumes, and demand for discretionary parts and components.

The 4 vehicle parts distributors stocks we track reported a strong Q4. As a group, revenues beat analysts’ consensus estimates by 2.9%.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 12.4% since the latest earnings results.

Rush Enterprises (NASDAQ:RUSHA)

Headquartered in Texas, Rush Enterprises (NASDAQ:RUSH.A) provides truck-related services and solutions, including sales, leasing, parts, and maintenance for commercial vehicles.

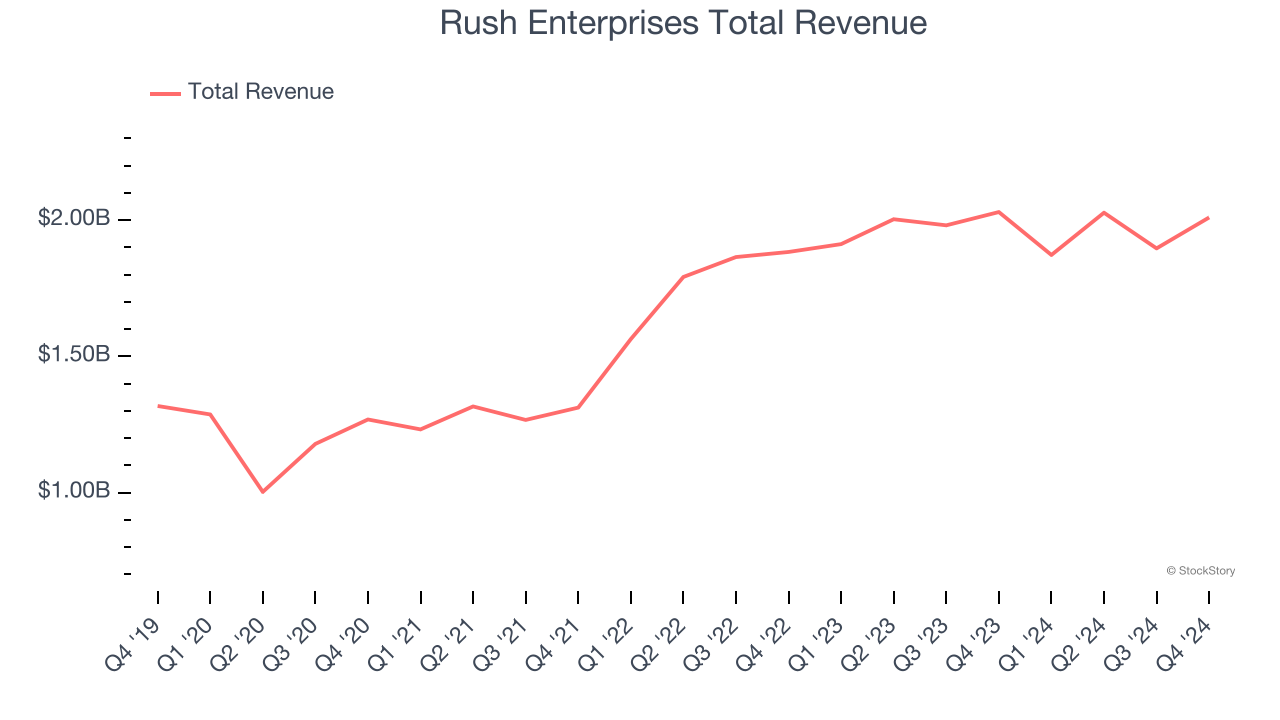

Rush Enterprises reported revenues of $2.01 billion, flat year on year. This print exceeded analysts’ expectations by 8.2%. Overall, it was a strong quarter for the company with an impressive beat of analysts’ adjusted operating income estimates and a decent beat of analysts’ EPS estimates.

“Despite the persistent headwinds the industry faced in 2024, I am proud of the financial results our team delivered,” said W.M. “Rusty” Rush, Chairman, Chief Executive Officer and President of Rush Enterprises,

Rush Enterprises pulled off the biggest analyst estimates beat but had the slowest revenue growth of the whole group. Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 14.9% since reporting and currently trades at $52.06.

Is now the time to buy Rush Enterprises? Access our full analysis of the earnings results here, it’s free.

Best Q4: Air Lease (NYSE:AL)

Established by a founder of Century City in Los Angeles, Air Lease Corporation (NYSE:AL) provides aircraft leasing and financing solutions to airlines worldwide.

Air Lease reported revenues of $712.9 million, flat year on year, outperforming analysts’ expectations by 1.6%. The business had an exceptional quarter with a solid beat of analysts’ EBITDA estimates.

Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 4.6% since reporting. It currently trades at $44.21.

Is now the time to buy Air Lease? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: FTAI Aviation (NASDAQ:FTAI)

With a focus on the CFM56 engine that powers Boeing and Airbus’s planes, FTAI Aviation (NASDAQ:FTAI) sells, leases, maintains, and repairs aircraft engines.

FTAI Aviation reported revenues of $498.8 million, up 59.5% year on year, exceeding analysts’ expectations by 0.9%. It was a satisfactory quarter as it also posted an impressive beat of analysts’ EBITDA estimates.

FTAI Aviation delivered the fastest revenue growth but had the weakest performance against analyst estimates in the group. As expected, the stock is down 28.2% since the results and currently trades at $100.69.

Read our full analysis of FTAI Aviation’s results here.

GATX (NYSE:GATX)

Originally founded to ship beer, GATX (NYSE:GATX) provides leasing and management services for railcars and other transportation assets globally.

GATX reported revenues of $413.5 million, up 12.2% year on year. This result beat analysts’ expectations by 0.9%. Overall, it was a strong quarter as it also produced full-year EPS guidance exceeding analysts’ expectations and a solid beat of analysts’ EPS estimates.

The stock is down 2% since reporting and currently trades at $151.44.

Read our full, actionable report on GATX here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.