As the Q3 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the agricultural machinery industry, including The Toro Company (NYSE:TTC) and its peers.

Agricultural machinery companies are investing to develop and produce more precise machinery, automated systems, and connected equipment that collects analyzable data to help farmers and other customers improve yields and increase efficiency. On the other hand, agriculture is seasonal and natural disasters or bad weather can impact the entire industry. Additionally, macroeconomic factors such as commodity prices or changes in interest rates–which dictate the willingness of these companies or their customers to invest–can impact demand for agricultural machinery.

The 6 agricultural machinery stocks we track reported a softer Q3. As a group, revenues missed analysts’ consensus estimates by 1.8% while next quarter’s revenue guidance was 11.1% below.

In light of this news, share prices of the companies have held steady as they are up 2.6% on average since the latest earnings results.

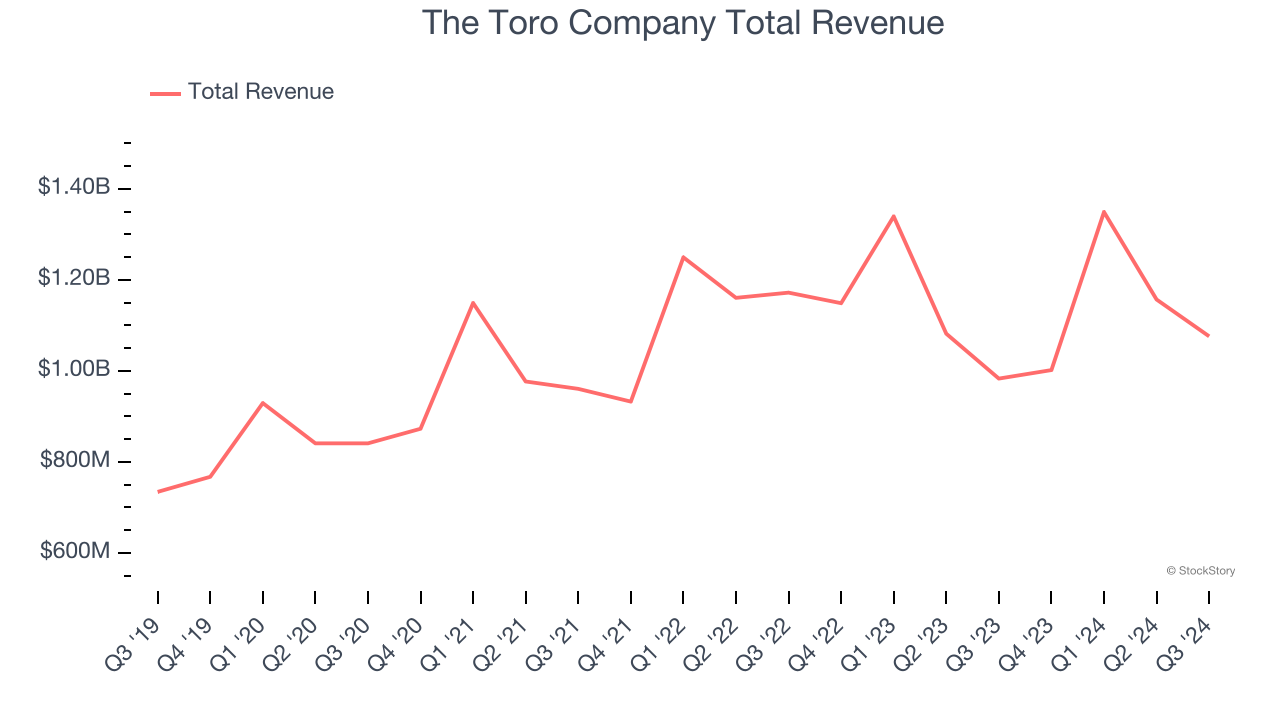

The Toro Company (NYSE:TTC)

Ceasing all production to support the war effort during World War II, Toro (NYSE:TTC) offers outdoor equipment for residential, commercial, and agricultural use.

The Toro Company reported revenues of $1.08 billion, up 9.4% year on year. This print fell short of analysts’ expectations by 1.3%. Overall, it was a disappointing quarter for the company with full-year EPS guidance missing analysts’ expectations.

“We delivered our 15th consecutive year of net sales growth in what remained an extremely dynamic environment,” said Richard M. Olson, chairman and chief executive officer.

Unsurprisingly, the stock is down 4.3% since reporting and currently trades at $81.65.

Read our full report on The Toro Company here, it’s free.

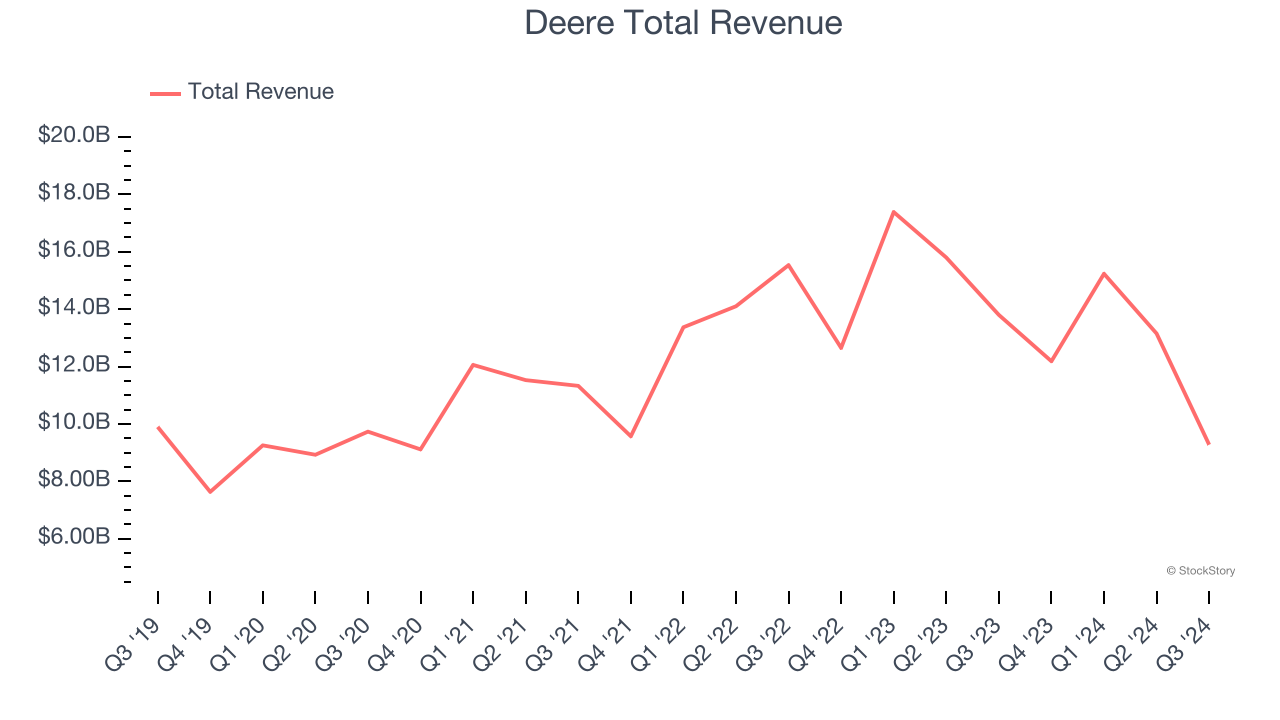

Best Q3: Deere (NYSE:DE)

Revolutionizing agriculture with the first self-polishing cast-steel plow in the 1800s, Deere (NYSE:DE) manufactures and distributes advanced agricultural, construction, forestry, and turf care equipment.

Deere reported revenues of $9.28 billion, down 32.8% year on year, in line with analysts’ expectations. The business had an exceptional quarter with a solid beat of analysts’ EBITDA estimates.

The market seems happy with the results as the stock is up 7.1% since reporting. It currently trades at $433.84.

Is now the time to buy Deere? Access our full analysis of the earnings results here, it’s free.

Weakest Q3: Titan International (NYSE:TWI)

Acquiring Goodyear’s farm tire business in 2005, Titan (NSYE:TWI) is a manufacturer and supplier of wheels, tires, and undercarriages used in off-highway vehicles such as construction vehicles.

Titan International reported revenues of $448 million, up 11.5% year on year, falling short of analysts’ expectations by 5%. It was a disappointing quarter as it posted full-year EBITDA guidance missing analysts’ expectations.

Titan International delivered the fastest revenue growth but had the weakest full-year guidance update in the group. As expected, the stock is down 5.8% since the results and currently trades at $6.94.

Read our full analysis of Titan International’s results here.

AGCO Corporation (NYSE:AGCO)

With a history that features both organic growth and acquisitions, AGCO (NYSE:AGCO) designs, manufactures, and sells agricultural machinery and related technology.

AGCO Corporation reported revenues of $2.60 billion, down 24.8% year on year. This number came in 10.4% below analysts' expectations. It was a disappointing quarter as it also recorded full-year revenue and EPS guidance missing analysts’ expectations significantly.

AGCO Corporation scored the highest full-year guidance raise but had the weakest performance against analyst estimates among its peers. The stock is down 4.3% since reporting and currently trades at $93.63.

Read our full, actionable report on AGCO Corporation here, it’s free.

Lindsay (NYSE:LNN)

A pioneer in the field of center pivot and lateral move irrigation, Lindsay (NYSE:LNN) provides a variety of proprietary water management and road infrastructure products and services.

Lindsay reported revenues of $155 million, down 7.3% year on year. This print surpassed analysts’ expectations by 6.5%. Aside from that, it was a mixed quarter as it also logged an impressive beat of analysts’ EPS estimates but a significant miss of analysts’ adjusted operating income estimates.

Lindsay achieved the biggest analyst estimates beat among its peers. The stock is up 13.9% since reporting and currently trades at $129.99.

Read our full, actionable report on Lindsay here, it’s free.

Market Update

Thanks to the Fed's series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market has thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% each in November and December), and a notable surge followed Donald Trump's presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by the pace and magnitude of future rate cuts as well as potential changes in trade policy and corporate taxes once the Trump administration takes over. The path forward is marked by uncertainty.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.